TLDR || Max out 401k (18,000 + 9,000 in match / free money || plus saving ~4500 in taxes) max out Employee Stock Purchase Program (ESPP) (25,000$ a year @ 10% off = 2,500$ in taxed extra money) Max out Health Savings Account (HSA) (6,750$ pre-tax ~1,600$ in tax savings)

Summary and stuff – why and short answer

Why write || I’ve been asked a few times over the last couple of years “how do you save” or “what do you invest in”

Simple Answer || I am obsessed with hording money and saving all of the things. I max out all pre-tax things, then save more. Right now about 31% of my income heads to company sponsored savings strait out of the paycheck via direct deposit. 401k, then HSA, then ESPP in that order due to taxes. Normally another 30% would end up in other savings accounts, but we built a house last year so some savings were paused and redirected the house. A month after 9/11/2001 I started work at John L Scott real-estate and made 55k a year. Since then I’ve never increased my take home pay to elevate my life style. Every increase in pay I’ve received since JLS has been diverted to savings. Last year I made 3x-4x my JLS wages.

401K Basics

2015 the Microsoft 401k was, Meh, with a 6% of salary match at 50 cents on the dollar. 2016 the Microsoft 401k is full on #baller status with a 50% match up to max level. I’ve always maxed out the 401k for the free money and tax savings. The match at Microsoft used to be an excuse to only put in 6%, 50% match removes all excuses. 50% match is a potential 9,000$ in tax free pay raise; I can’t imagine an excuse strong enough to not get this pay raise. When you add in the tax savings at an average 25% tax bracket on the income you’re saving about 4,500$ a year in federal income taxes. In real money the 9,000$ in free money only costs you 13,500 or about 1,100$ a month to make an extra 750$ a month.

Time is power and a force multiplier with investing. I like for max level return on my investments so I attempt to max out my 401k as soon as is comfortable for the year. This year the goal is to hit max level around August / September then the money be allocated to backdoor Roth conversion magic.

Math and stuff

| Cost | – 18,000 a year @ 1,500$ a month |

| Tax Savings | + 4,500$ federal tax savings / 375$ a month tax savings |

| MS Match | + 9,000$ |

| Actual Cost | -13,500$ a year @ 1,125$ a month real cost to pay check |

| Total Gains | +27,000$ a year in tax free savings + 4,500$ less tax paid |

Best Advice to save more ||

If you cannot max level now, then add 1% every 3-6 months. 1% is maybe 100$ a month / 50$ a pay check. It’s a small enough amount you won’t notice it coming out of your budget. It’s a large enough amount you’ll notice it in 30 years.

What to Invest in

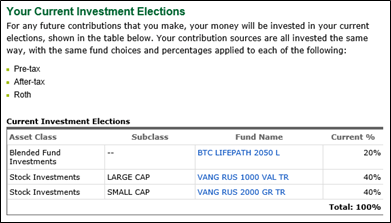

I’ve never had an issue with risk, the more the better. I’m also younger and have time on my side, so I go for the higher risk higher gain potential gains. I’m also pretty gosh darned frugal, so I go for the cheapest funds possible. This month, those two requirements mean I’m in three funds offered available in the plan.

The Blended fund is based on age of when you expect to retire and it does its own asset allocation based on that age. Meaning it is more aggressive now and becomes less aggressive heavier on bonds as the retirement age approaches. If you don’t know what to do putting everything in one of these is not a horrible idea

HSA Basics

In 2016 the HSA limit is 6,750$ a year. HSA contributions are pre-tax, meaning they come out before you are charged income tax like the 401k. Contributing the max level of 6,750$ a year into your HSA account saves you 1,600$ a year in federal incomes taxes at a base rate of 25%. In terms of real income saved the HSA contribution only costs you 5,150$ of usable income. The Premera HSA has a number of low cost vanguard mutual funds you can invest your money in every time there is more than 150$ in your account.

My goal is max money in the HSA at retirement. I want to use the returns from HSA investments to pay for my medical expenses in the future. You’re limited on how much you can put in the HSA, so, In the present we pay all of our medical expenses out of pocket and leave the HSA money in the investment account to grow.

Note || I write these posts in Word 2016, and word has autocorrected HSA into HAS every bloody time – mutter. I blame Les; he’s notorious for picking on me like this.

ESPP Basics

The ESPP is not as slam dunk of a sale. It’s only a 10% taxed gain on your money with a 3 month holding cost, but free money is free money. I have a difficult time passing up from money. Microsoft ESPP Microsoft takes X% out of each paycheck and holds it for a quarter. At the end of the Quarter Microsoft gives you Microsoft stock at 10% off the cover price. You are free to sell the stock on the day it hits your account.

The first logical justification of the ESPP for me is annual, or semiannual bills. For us that’s our homeowner’s insurance, property taxes, and income taxes [1]. The next justification is my play account of 500$ a month. If I can afford to play less for 3 months for the first round, then I get 1,650 to spend over the next 3 months to play with. More money to play with at the same out of pocket cost is not a difficult sale. I mix the ESPP into two buckets; Cover expenses, and invest with starting by writing covered calls.

Josh Maher explains covered calls far better than I can with his covered calls category and his step by step how to sell covered calls on ESPP.

A few more words

If you max out 401k, and HSA, and ESPP then you’re dominating the saving game above about 95% of the US population, and it would be high improbable to not retire well. Disclaimer, I’m sure it’s still possible to screw up picking the wrong funds, taking money out, leaving things in cash, ETC, but the chances are slim. What works for Michelle and I might not work for you. We’re pretty frugal people and don’t need much. Between the two of us we drive about 7,000$ in cost to us cars, and maybe spend 400$ a year on clothing including a few new pairs of shoes Microsoft pays me back for.

Another big part of what I do is it’s on auto pilot, and I save first before income touches my spending accounts. The bulk of my monthly investments happen without any action on my part, and most times I don’t even notice them because I don’t look at my pay stub. Saving is a part of my life that happens no matter what stress is taking place, or how much attention I’m paying to it. I save before paying myself.

[1] We claim 10 on W4 Thinking we’d rather pay at income tax time and have more money to manipulate vs. letting the government have a tax free loan.

{kind=link}

{kind=link}

{kind=link}

{kind=link}